When Should You Take Social Security? It Depends on More Than Your Age.

One of the most common questions I hear from clients in their late 50s and early 60s is some version of this: when should I take Social Security?

It sounds like a simple question. The answer is not (which is why this blog is a long one).

The decision about when to claim Social Security benefits is one of the most consequential retirement income planning choices you will make. Get it right, and it can add tens of thousands of dollars in lifetime income. Rush it without a plan, and you may leave a significant amount on the table permanently.

Here is what the decision actually involves, and how to think through it clearly.

Quick Takeaways

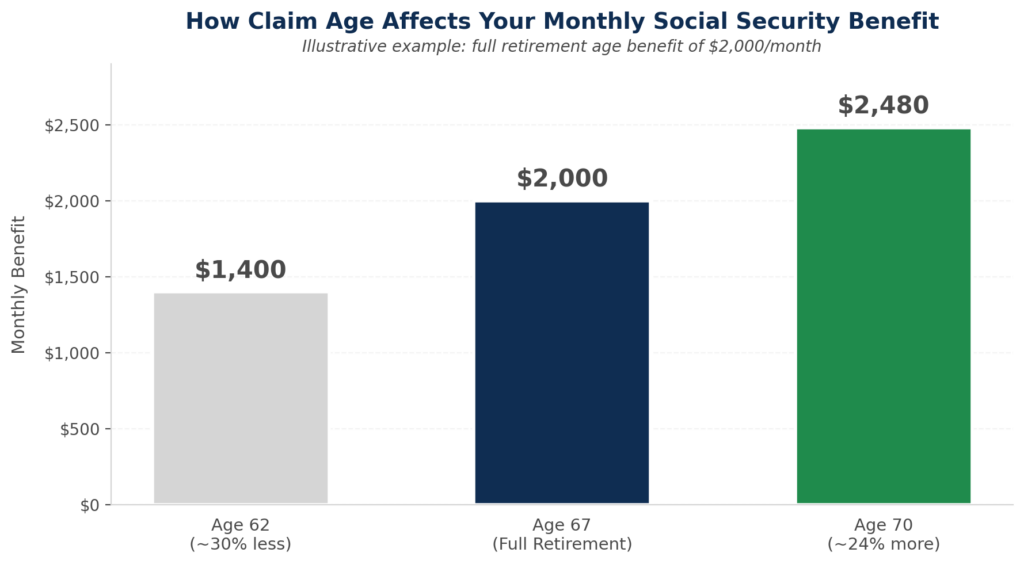

- Claiming at 62 reduces your benefit by approximately 30% for life. Waiting until 70 increases it by 24%.

- For couples, the higher earner’s claiming age often matters more than break-even math suggests, because of the survivor benefit rule.

- Coordinating Social Security with Medicare premiums, taxes, and retirement withdrawals can meaningfully change the outcome.

- If you are within ten years of retirement, this decision belongs in your plan now.

How Social Security Benefits Are Calculated

Your Social Security retirement benefit is based on your earnings history, specifically your average indexed monthly earnings across your 35 highest-earning years. The Social Security Administration uses that figure to calculate your primary insurance amount (PIA), which is the benefit you receive at full retirement age.

Full retirement age is 67 for anyone born in 1960 or later. You can begin claiming as early as 62, but doing so permanently reduces your monthly benefit. For each month you claim before full retirement age, your benefit is reduced by a small fraction. Claim at 62, and the reduction is approximately 30%.

Wait past full retirement age, and your benefit grows by 8% for each additional year you delay, up to age 70. That is an inflation-adjusted increase set by federal law that is difficult to replicate anywhere else.

Here is what that looks like. If your full retirement age benefit is $2,000 per month, claiming at 62 would reduce your monthly check to roughly $1,400. Waiting until 70 would push it up to about $2,480.

That is more than $1,000 per month, for the rest of your life, depending on when you claim. For couples, the stakes are even higher.

The Break-Even Question

Most people approach this as a break-even analysis: at what age does delaying actually pay off? If you claim at 62 instead of 67, you receive more money in your early retirement years. But every month you collect early, you collect less.

At some point, usually in your late 70s or early 80s, the cumulative benefit of the person who delayed surpasses the one who claimed early.

The break-even point matters, but is not the only thing to consider.

Your health and life expectancy are real inputs. If you have a strong family history and are in good health, delaying looks more favorable mathematically. If health concerns suggest a shorter timeline, claiming earlier may make more sense.

Your income needs matter too. If you have other income sources, like a pension, investment portfolio, rental income, or a working spouse, you may be able to bridge the gap while allowing your Social Security benefit to grow. If Social Security is your primary income source, the calculus looks different.

Taxes add another layer. Social Security benefits are taxable if your combined income exceeds certain thresholds. Higher-income retirees can find that claiming early creates a tax burden that erodes the benefit more than the raw numbers suggest.

There is also a temporary tax benefit worth knowing about. The One Big Beautiful Bill Act, signed into law in July 2025, created a new $6,000 deduction for taxpayers age 65 or older, available through the 2028 tax year. Married couples where both spouses qualify can claim up to $12,000.

The full deduction is available to single filers with modified adjusted gross income up to $75,000 and joint filers up to $150,000, and phases out completely at $175,000 for individuals and $250,000 for couples. Higher-income retirees will not see the full benefit, but for those in or near the phase-out range, this deduction can shift the after-tax math during the years it is in effect.

Spousal Benefits and Survivor Income

For married couples, Social Security claiming strategy gets significantly more complex. It also gets significantly more important.

Each spouse has their own benefit based on their individual earnings history. A lower-earning spouse can claim up to 50% of the higher-earning spouse’s benefit if that amount is larger than their own. This spousal benefit is only available once the higher-earning spouse has filed.

Key Insight for Couples

When the higher-earning spouse passes away, the surviving spouse receives the higher of the two benefits, but only the higher one.

If the higher earner claimed at 62, the survivor inherits that reduced amount for the rest of their life. This is why delaying the higher earner’s benefit often matters more than maximizing total household income today.

This is why the most common recommendation for married couples is for the higher earner to delay as long as possible, while the lower earner may claim earlier. Delaying the higher benefit grows survivor income, which is one of the most important factors in long-term retirement income planning for couples.

Coordinating two Social Security claims requires running the numbers carefully for your specific ages, benefit amounts, health considerations, and income needs. The right answer for one couple is not the right answer for another.

What Happens If You Claim While Still Working

If you are still working when you become eligible at 62, claiming Social Security early is usually not a good idea.

Before you reach full retirement age, the Social Security earnings test applies. If your earned income exceeds a certain annual threshold ($24,480 in 2026), your benefits are temporarily reduced by $1 for every $2 earned above the limit.

Those withheld benefits are not lost permanently. They are added back to your future benefit once you reach full retirement age. The temporary reduction creates cash flow complications that most people want to avoid.

Once you reach full retirement age, the earnings test disappears entirely. You can work and collect full benefits with no reduction.

The takeaway: if you plan to keep working, waiting until at least full retirement age before claiming typically makes more sense, both financially and administratively.

Medicare Timing and Income Surcharges

Medicare eligibility begins at 65, and it is connected to Social Security in ways that affect your retirement income planning, particularly if your income is higher.

Medicare Part B and Part D premiums are income-based. Higher-income beneficiaries pay a surcharge called IRMAA, the Income-Related Monthly Adjustment Amount.

2026 IRMAA Thresholds

Individuals: modified AGI above $109,000

Married couples: modified AGI above $218,000

The surcharge can add hundreds of dollars per month to Medicare costs.

This matters for Social Security claiming strategy because the income used to calculate IRMAA is based on your tax return from two years prior. A Roth conversion, a large IRA withdrawal, or a business sale in a given year can trigger higher Medicare premiums two years later. That timing can overlap with when you are starting to claim Social Security.

Coordinating the timing of Social Security, IRA withdrawals, and Roth conversions with Medicare premium calculations is an area where professional guidance typically pays for itself.

Social Security as Part of Your Retirement Income Plan

Social Security is one source of retirement income. It is not a complete retirement income plan on its own, and optimizing it in isolation misses the point.

The most effective Social Security claiming strategies are built around the full picture: what other income sources you have and when they start, what your spending needs look like year by year, what your tax situation will be in retirement, and how your portfolio is structured to support withdrawals.

In some cases, spending down portfolio assets in the early years of retirement while delaying Social Security produces the best long-term outcome. In others, claiming earlier and leaving portfolio assets invested to compound is the better path. The right answer depends on your specific numbers.

At Heritage Wealth Solutions, retirement income planning covers all of it: Social Security timing, investment drawdown strategy, tax positioning, and long-term income sustainability. The goal is a plan that works across your full retirement, not just in the first few years.

When to Start This Conversation

The Social Security claiming decision does not have to be made the moment you become eligible. It should be made intentionally, with time to model the scenarios and coordinate with the rest of your plan.

If you are within ten years of retirement, now is a good time to start thinking through your Social Security claiming strategy. The earlier you build this into your plan, the more options you have, and the less likely you are to make a decision that reduces your lifetime income because you needed the money in the moment.

Questions about when the right time to claim is for your situation?

We are glad to walk through it with you.

Or call us at 602-833-4300

Material in part created with Claude.

Every investor’s situation is unique and you should consider your investment goals, risk tolerance and time horizon before making any investment. Prior to making an investment decision, please consult with your financial advisor about your individual situation.

The foregoing information has been obtained from sources considered to be reliable, but we do not guarantee that it is accurate or complete, it is not a statement of all available data necessary for making an investment decision, and it does not constitute a recommendation. Any opinions are those of Chris Hilyer and not necessarily those of Raymond James.

You should discuss any tax or legal matters with the appropriate professional.